In the UAE, your credit score quietly influences many parts of your financial life. It affects whether you get a loan, the limit on your credit card, the interest or profit rate you’re offered, and sometimes even how smoothly a bank account is opened. Many residents only discover its importance when an application gets rejected without a clear explanation.

By 2026, credit scoring in the UAE has become stricter, more data-driven, and more widely used by banks and finance companies. Understanding how it works—and how to improve it—can save you money and prevent unnecessary stress.

What Is a Credit Score in the UAE?

A credit score is a numerical summary of your credit behavior. It reflects how responsibly you use financial products like loans, credit cards, and buy-now-pay-later services.

In the UAE, credit scores are issued and maintained by Al Etihad Credit Bureau (AECB). All licensed banks and financial institutions report customer data to this bureau.

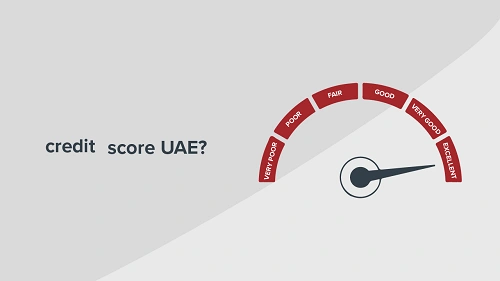

The score typically ranges from 300 to 900:

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800–900: Excellent

The higher your score, the lower the perceived risk you present to lenders.

How the UAE Credit System Works

Unlike some countries where credit history starts early, many people in the UAE begin with no score at all. Your credit profile only starts building once you use a regulated financial product.

Banks and lenders regularly report:

- Credit card usage and limits

- Personal, auto, and home loans

- Payment history (on time or late)

- Outstanding balances

- Defaults or write-offs

This information is compiled into your credit report, from which your score is calculated.

What Affects Your Credit Score the Most?

While AECB does not publicly disclose its exact formula, the key factors are well understood.

1. Payment History (Most Important)

Late payments are the biggest negative factor.

Even:

- A few days’ delay on a credit card

- One missed EMI on a loan

can significantly damage your score. Repeated late payments compound the damage.

2. Credit Utilization Ratio

This refers to how much of your available credit you actually use.

Example:

- Credit limit: AED 50,000

- Used balance: AED 45,000

This high usage signals risk, even if you pay on time. Ideally, you should use less than 30–40% of your available limit.

3. Length of Credit History

The longer your active, well-managed credit history, the better. Closing old accounts can sometimes hurt your score because it shortens your history.

4. Credit Mix

A healthy mix helps:

- Credit cards

- Personal loans

- Auto or home finance

Relying only on credit cards or only on short-term loans can limit your score potential.

5. New Credit Applications

Each loan or card application triggers an inquiry. Too many applications in a short time make lenders nervous and can reduce your score.

How to Check Your Credit Score in the UAE

You can legally check your own credit score without harming it.

Through Al Etihad Credit Bureau, you can:

- Request your credit report

- View your score

- See detailed account history

This usually involves a small fee and identity verification using Emirates ID.

Checking your own score is considered a soft inquiry and does not affect your rating.

Common Myths About Credit Scores in the UAE

“No loans means good credit.”

False. No credit activity often means no score at all.

“Salary decides credit approval.”

Salary matters, but a poor credit score can still lead to rejection.

“Once damaged, it can’t be fixed.”

Also false. Credit scores can improve with consistent behavior.

How to Improve Your Credit Score in the UAE

Improving your credit score is not instant, but it is predictable if done correctly.

1. Pay Everything on Time

Set up:

- Auto-debit for loans and cards

- Calendar reminders

Even one late payment can undo months of progress.

2. Reduce Outstanding Balances

If your cards are near the limit:

- Pay them down gradually

- Avoid maxing out cards again

Lower balances improve your utilization ratio quickly.

3. Don’t Close Old Credit Cards Unnecessarily

An old card with good history helps your score—even if you don’t use it often. Keep it active with small transactions paid off monthly.

4. Limit New Applications

Apply only when necessary. Multiple rejections harm both your score and your banking profile.

5. Correct Errors in Your Credit Report

Mistakes happen:

- Closed loans shown as active

- Incorrect late payment records

You can dispute errors directly through AECB with supporting documents.

6. Use Credit Responsibly, Not Avoid It

If you have no credit history:

- Start with one low-limit credit card

- Use it monthly

- Pay in full before the due date

This builds a positive record safely.

How Long Does It Take to Improve a Credit Score?

- Minor issues: 3–6 months

- Serious delinquencies: 12–24 months

Negative records don’t disappear overnight, but their impact reduces over time if your recent behavior is strong.

Why Credit Score Matters More in 2026

In recent years, UAE banks have tightened risk controls. Automated systems now screen applications before human review.

A good credit score can mean:

- Faster approvals

- Higher loan limits

- Better interest or profit rates

- Easier refinancing

A poor score can silently block opportunities—even if your income is strong.

Final Thoughts

Your credit score in the UAE is not a judgment of wealth or status. It’s a reflection of habits. Small, consistent actions matter more than big, occasional ones.

Pay on time. Keep balances low. Apply wisely. Monitor your report.

By 2026, credit scoring is no longer a background system—it’s a gatekeeper. Understanding how it works gives you control over your financial options and helps you build long-term stability in the UAE.